#139: Duration thoughts, and a little Marie Kondo

#139: Duration thoughts, and a little Marie Kondo

April 7, 2024; 17 minute read - 42% finance, then 58% about joy in real life

Serious finance

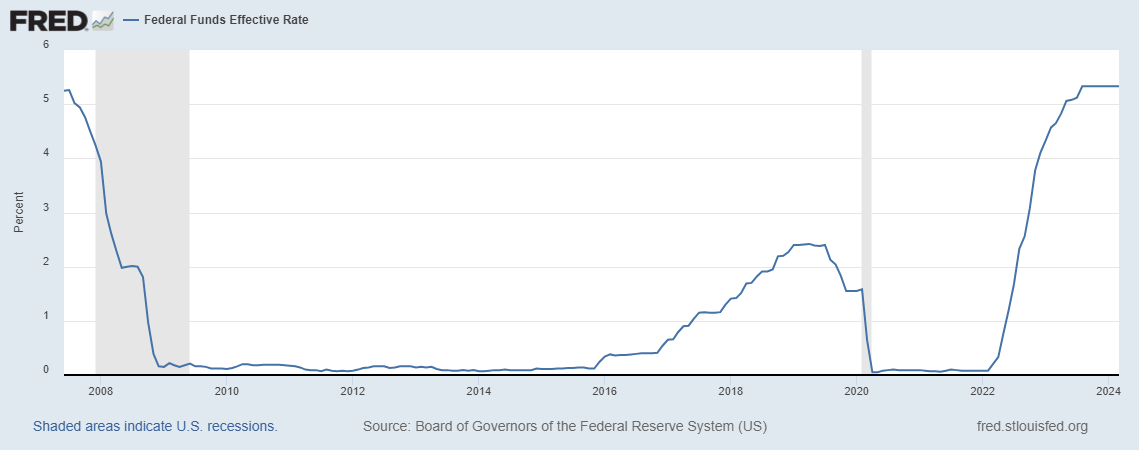

I’ve been thinking a lot about duration lately, but in a fuzzy way. Technically, in finance, duration is a measure of the interest rate sensitivity of a (bond) portfolio. I have been using it more in the sense of “investment horizon,” because interest rates and therefore central bank policy have a great deal of influence over ‘optimal’ investment horizons. More simply, it’s a kind of a measure of how long it would take to get your money back.

During a low- to zero-rate environment (like the period 2009-2022 in the US, depicted above), long duration (investment horizon) strategies become more attractive, because low interest rates essentially value income in future years similarly to current income — so the ideal investment was something which would grow at a fast rate, for a long number of years. To be precise, very low short term interest rates had the effect of driving down medium and long term rates as well (the US 10 year yield was under 1% for most of 2020); the entire interest rate curve has rebounded as central banks have normalized short term rates.

This prolonged low interest rate environment facilitated a variety of literal moonshots and “build it and they will come” ventures, which could take years or even decades to develop — these strategies would not be possible with higher (more normal) interest rates. As interest rates fell off a cliff and remained low, this stimulated a rush of talent and capital into long duration growth businesses, like startups and real estate, as well as the related asset management spaces of private equity and venture capital. This long duration wave drew both human and financial capital from more short duration businesses like traditional banking and consulting. Importantly, this did not affect all regions equally, as the effect was concentrated in places with existing high growth cultures, like Silicon Valley. Japan has had low interest rates for many decades but without a dynamic growth culture, the result of three decades of near-zero rates has been far less pronounced.

Like many other financial lemmings, I followed the burgeoning wave as well, leaving investment banking in Asia, moving to long duration Ground Zero (the San Francisco Bay Area), making a variety of long term investments into startups from 2015 (five years too late), and eventually working at an aerospace startup with an audacious mission and an increasingly long time horizon.

But interest rates didn’t stay at zero forever — they normalized with a vengeance in 2022-23. A half-hearted attempt at a recovery was made from 2016 but US policy rates only got to 2.5% (still quite low, compared to history) before COVID threw a mask on the recovery and we had another three years of zero interest rates.

Now that US policy rates are above 5% (and even Japan has raised rates for the first time in over two decades), I’m venturing back to the short duration universe of more traditional finance, which has attracted less attention for some time.

Duration and liquidity

Invariably, when interest rates fall precipitously, there is an onslaught of capital moving towards long dated growth, because the low interest rates essentially value future income similarly to current income; this usually drives large price increases in these asset classes. The opposite effect occurs when those low rates normalize, and these assets depreciate.

Except there is one important difference: the asymmetric liquidity function.

Another word for liquidity is tradability: short duration assets almost always have ample liquidity because by definition they mature in the near term. If I have a long duration asset where there is a liquid tradable market, then I can dispose of the asset for cash at any time (and get all or most of my money back). Instruments like 10Y government bonds are well-traded with excellent liquidity; REITs are essentially real estate derivatives which are often listed and traded, even if their underliers are not traded frequently. Equities have no maturity at all (they are essentially perpetual), but large cohorts of equities are listed on exchanges and traded regularly. However, to be listed, an equity generally needs to be a mature, profitable, ongoing concern with stable or growing revenues and profits.

But many long duration assets are not tradable: (largely unprofitable) startups are unlisted and mostly untradable, and investor (LP) stakes in venture capital or private equity are also essentially non-tradable (even if some of the PE funds are listed themselves). Indeed, one of the major objectives of any startup is to become listed (an ‘exit event’), a sign that it has survived the high risk phase to reach the status of a profitable ongoing (and liquid) concern, something which drives distributions to private equity and venture capital investors.

Physical real estate is generally viewed as a long dated asset, but with relatively poor liquidity for a variety of reasons, including very large deal sizes, and the uniqueness of each real estate asset. In fund or derivative forms, real estate liquidity can be increased. Privately negotiated real estate deals are done periodically, so they are more liquid than equity in the average growth startup.

When interest rates are going down, and exciting long duration assets are inflating, liquidity is generally excellent as investors pile in. But when the markets turn down and investors get spooked, liquidity tends to disappear, and extracting cash becomes devilishly difficult. For most startups, expenses dwarf revenues, so they continue to require investment capital to continue their quests, but even existing investors become wary of adding to their long dated portfolio. In real estate, the underlying leases and loans are long dated so the physical assets don’t reprice frequently.

The lack of liquidity affects other variables, as partially noted in this recent lament about the private equity world, and this one from the Wall St Journal: in order to generate liquidity, either the price moves down (considerably), or duration gets even longer (so risk essentially increases because of an unwillingness to break price). When a startup runs out of cash and closes down, the asset disappears and investors lose most or all of their investment.

Typically, for most low liquidity long duration assets, what happens is that a chasm develops in the spread — the price between what buyers are willing to pay, and what sellers are willing to accept, so very little trades — over time it is usually the desperate sellers who capitulate, first individually, then en masse. Once the dam breaks, the buyers lower their bids even further (“don’t catch a falling knife”). If defaults occur and collateralized assets revert to their banks, it can create a fire sale atmosphere, catalyzing rapid downside (while helping liquidity by creating large discounts).

The common lament for low liquidity long duration investors is a financial analogue to Schrödinger’s cat (the confused cat is both alive and not alive at the same time) — asset rich on paper, but simultaneously cash flow poor.

The Wall St Journal noted here that many US office rents haven’t collapsed in general despite record high vacancies — and in fact some of them are going up (other than San Francisco, where the situation is harder to sugarcoat). Behind the scenes, of course, special offers abound, like up to a year of free rent, or inclusive of expensive buildouts, because owners are eager to keep nominal rents to maintain their assessed property values, while offering substantial back room incentives to attract jittery price conscious tenants.

This dearth of liquidity can afford opportunities for those with cash: startups on the precipice of the next milestone, desperate to salvage some of the value they created, may agree to onerous financing terms and discounted valuations because they have few other choices. From most insider accounts, the repricing of global startups is well underway but is far from over, given the natural resistance of founders and stakeholders towards down rounds. Similar dynamics work in the real estate market, with the added dimension of debt, so price moves can be magnified because of the leverage.

So even though US policy rates have been over 5% for a while now, the lack of liquidity (and transparent pricing) for illiquid long dated assets like startups and real estate suggest a painful path to find tradable prices. In the zero-rate environment, the common wisdom was cash (demand deposits) “sucked” because the banks paid next to nothing for them; when the cycle reverses, cash (and cash flow) become ‘king’ again, and having a surplus of cash generates good income and also allows the option to buy long dated assets at distressed prices.

So it turns out I’m not really perspicacious in my strategic thinking, I’m just following the incentives of the rate cycle, like a very ordinary cud-chewing bovine. Now that I’m prioritizing cash flow, I’m moving to the short end of the duration spectrum.

Perhaps unsurprisingly, my musing about the duration measure stimulated some thinking about analogues in other realms.

Marie Kondo: duration and joy

As I mentioned in my last issue, I’m in the process of moving my accumulated junk across the Pacific, and thinking a lot about Marie Kondo. While the concept of duration in finance can’t be applied directly to things, I think the analogue might be ‘relevant useful period’ – and in practice, the financial world uses 3 years as the dividing life span between ‘durable goods’ (LED TVs, Hermes bags, etc.) from ‘fast moving consumer goods’ (FMCG: most food, toilet paper, etc.). I’m not sure where Spam would go.

Durable items generally have very long theoretically useful lives, and that the owner largely determines their end point (give away, sell, throw away, destroy, get stolen). When we purchase items, we rarely consider that this item will basically last forever, until I get rid of it somehow. Thus we accumulate all sorts of long duration items until we are living in a personal warehouse. Electronics (particularly phones and computers) are a special case: their relatively short useful life is determined by the rapid rise of better alternatives, especially if they are engineered to slow down by the manufacturer to accelerate the upgrading process.

The near immortality of things is amplified for important items like furniture or artwork, because they are psychologically harder to throw away (the sunk cost fallacy), but they are also difficult to sell. When we are starting out after college, we need some furniture but have a small budget and little idea what our lives might look like in the future (to inform what kind of items will serve us best for a long period of time). Fortunately, furniture doesn’t have a carrying or maintenance cost, it just sits there until it’s time to move (there is an indirect moving cost). But there’s also an opportunity cost, if you have a major piece, it generally precludes being able to buy any other similar piece (unless your real estate portfolio grows), and sometimes it requires long term storage. Thinking back, one of my best silver lining events was a result of my divorce: I lost an entire apartment’s worth of furniture, and kept only a single daybed, which I happily use to this day. I can’t imagine what I’d do these days with three dainty matching sofas in crimson damask.

Why the theta measure is important

In options theory, we use a variety of Greek letters to denote different options parameters (sensitivities). Among these, theta (usually a negative value) is a measure of how much an option changes in value with respect to time — carrying costs, essentially. For my large furniture items, the primary source of theta are my periodic moving costs (and sometimes storage costs), which I tend to do every 3-5 years.

For certain classes of goods, like fine wine, their value fluctuates over time, rather than merely depreciating. In wine, each varietal and vintage has different aging functions — classic red wines tend to improve over time, maturing into balanced and multi-dimensional experiences, then after an inflection point, the oxidation process eventually renders them less pleasing. For white wines, this process happens more quickly, as I recently realized when my inventory showed a disturbing number of Gloria Swansons (in Sunset Boulevard): cases of old white Burgundies which, once excellent, are now passing their prime and warrant immediate drinking. For all wines, another source of theta is the cost of storage, either professional storage, or the cost of wine fridges, which can be considerable. In fairness, my wine has tended to appreciate over time (a pleasant but incidental surprise), more than offsetting the storage costs, so the net theta has been quite positive. And since there is a liquid market to resell fine wine (and even price indices), it is possible to change the duration of the asset.

I suppose Marie Kondo would argue that an item could have positive theta if it gives you great joy everyday (like my day bed). However, Kondo-san doesn’t opine on how much joy an item should give you (minimum standard joy, or MSJ), the duration of the joyful period, the intensity of the joy, or even aggregate joyousness relative to an item’s carrying cost. We all agree that zero joy possessions should be excised.

We rarely use the large part of our possessions — and this goes double for items which belong to our non-primary residences. Indeed, some of our possessions we only handle when we move — while we are resident in any one place, we hardly handle or notice them at all, making it an enigma that we feel a need to keep them with us. Many of our books are in this category – they last forever, we rarely handle them, they are heavy, and they take a concerted effort to process. By comparison, we don’t use spices very much either — they probably don’t give us joy every day but they inject joy into unspiced dishes, and at least they don’t weigh a lot or take up much space.

Artwork is in a different class altogether — most of our possessions empirically decline in value but artwork has the remote possibility of going up over time — even if we never resell it, there is some pleasure in buying something before it becomes unaffordable. Because it is possible to interact with art every day, albeit momentarily, and art ideally has an emotional rather than practical function, there might be more associated joy with art works, even if there is a spectrum, from functional pieces to liven up a wall, to bona fide heirlooms. Nowadays I ask myself how long am I likely to be enamored of this work, so my habits have gravitated to what I consider timeless more than intriguing/quirky (or so I tell myself).

I’m guessing we tend to be more rational about much larger ticket items like cars, boats, and residences, for instance — because the stakes are high enough that we’re incentivized to be rational, and in many cases the negative theta is considerable and catalyzes the disposal process.

Relationship durations

I suppose the idea of duration can apply to relationships as well, even though I’m aware this seems a little heartless. People come and go from our lives, it’s hard to tell how long someone will be close to us (as mentioned in my analysis of my Dunbar cohort in CoV #72).

In the normal course of events, your immediate family will generally have the longest durations (as well as the most frequent and intense interactions). It goes without saying that the highest positive theta values accrue to your parents, the people who give you life, bring you into this crazy Earth, and who nurture, feed, and educate you from a helpless blob until you reach a modest level of self-sufficiency; then humor and support you even after you leave the proverbial nest.

We are biologically programmed to derive great positive theta from our children, even as taking care and dealing with them (especially as teenagers) can rack up stinky piles of negative theta. Our children make us pseudo-immortal, because they acquire some of our unique DNA, and they can recursively pass these fractional genes along. This idea must be quite comforting for those of us lucky enough to have progeny. I suppose grandchildren have the best theta balance, because grandparents derive joy from their existence and cuteness, but do not have the responsibility of raising them — there’s no wonder that they are a more unilateral source of happiness.

Friends will drift in and out: BFFs are rarely forever, and as you cycle through phases, so too does your friend cohort morph along with you. The frequency function for friends can change a lot — there is usually the intense period of shared time together (school, university, work, etc.) followed by an after period in which interaction frequency usually drops off considerably. Fortunately friends are not singular — ideally, one will have a dynamic bouquet of friends which will slowly change over time.

Serious relationships — potential life partners — have higher stakes, because the (usually exclusive!) interaction is intense and the frequency is high — but in reality, neither party really knows the actual duration of the relationship. Compared to friends, which are lower stakes interactions, the duration parameter of one’s significant other is of critical importance, but is often vastly overestimated, highly dynamic, and therefore sadly unknowable.

The dimensions of interaction frequency and intensity are important to round out the variables of duration and theta — somewhere in this, there’s an equation lurking, some sort of integral of duration x (frequency*intensity + net theta) — but it seems pretty silly to create a human interaction analogue to a discounted cash flow (DCF) formula. The larger point is that duration and theta are not enough, that the frequency and intensity of interaction must also be considered as well — in addition to other factors I have probably overlooked (the opportunity cost of time, perhaps).

Relating this to life editing

My last issue was about taking a more active role in editing one’s life — this is an admittedly cold hearted (but practical) approach to assessing what belongs and what should be deprecated. We largely do this already, we just don’t actively think about the dimensions of duration and theta. We spend more time with friends we find amusing and relevant, we remove toxic and untrustworthy elements, we adapt to circumstances and modify our environments.

A few years back, I decided that one of my cousins was insufferably annoying, and that I would refuse to have any more to do with them. Relatives are passively allotted to us — we have no active role in selecting them (I’m not counting children) — and therefore there should be less of a regret function because they are not active choices. In this case, announcing my decision to my immediate family felt very liberating — although the interaction frequency was low, the theta was always negative, and the family connection meant that the (somewhat obligatory) duration was long. So I made a choice to spend time with relatives who I actively like and enjoy, and zero time with the isolated human Love Canals that happen to be in the family.

With regard to little used possessions, most of us keep them around longer than we should — getting rid of them is often a pain, and we tend to overestimate how much we’ll use them in the future. Sunk cost fallacy works here too — the more expensive the item, the less likely we are to part with it, because it represents something between imprudence and outright bad judgment — unless we can manage to sell the item. But with possessions, in contrast to friends, where there is a social dimension, we can be more dispassionate in our assessments because our possessions don’t have feelings if and when we no longer need them.

Final words

Duration and liquidity can help explain some of the macro trends in the investing world, but moving towards long duration assets should always include an assessment for the asymmetry of liquidity risk, which is not trivial. And the duration concept might be useful in other areas.

Within the world of objects, a duration perspective that includes theta, frequency, and intensity is just another loose framework, a way of partially reconciling options theory to the world of Marie Kondo. Theta is usually more explicit because we can measure it day-to-day — Kondo-san focuses on a simplistic equation of “whether something gives you joy” — but not in relation to its potential duration or carrying costs, to say nothing of frequency and intensity – thus I would argue that her single variable binary equation is short sighted (but a useful shorthand measure).

The framework needs modification with regard to relationships, because there are so many factors to consider, and the frictional and societal costs of removing someone from your network can be non-trivial. That doesn’t mean it shouldn’t be done – some people take advantage of those frictional costs to abuse a relationship, but the decision to change someone’s status should not be taken lightly. Our estimates of relationship duration are often far off the mark, and need to be revised periodically.

The upshot of this exercise is to consider duration with respect to one’s career, but also about who and what to include in our finite duration lives — now with a rough framework to think about what factors drive those choices.

[I promise my next issue will be more lighthearted.]